VAT Return UAE – Things To Know Before VAT Filing in UAE

VAT Return in the UAE is a mandatory tax filing for businesses to report VAT collected and claimed. Learn key steps, deadlines, and common mistakes to ensure smooth VAT filing in the UAE.

Table of Contents

Let's Talk

Sign Up For Free Consultation

VAT Returns in UAE: Essential Guide Before Filing Your VAT

If you’re a Taxable Person in the UAE, understanding the VAT Return process is essential to ensure compliance with the Federal Tax Authority (FTA). Filing VAT Returns accurately and on time can save you from penalties and enhance your business credibility. At Tulpar Global Taxation, we specialize in guiding businesses through the complexities of VAT UAE, from preparing VAT Return forms to validating financial records. Whether you’re managing taxable supplies, zero-rated supplies, or claiming input VAT against your output VAT, staying compliant is critical to your success in 2026 and beyond.

The UAE’s tax refund system allows businesses to recover VAT paid on eligible expenses under the refund scheme. However, to claim a VAT refund, businesses must properly maintain their financial records and ensure that all entries align with added tax regulations. Filing VAT for the correct tax period requires accurate validation of the VAT amount, ensuring all taxable and non-taxable transactions are properly recorded. By partnering with Tulpar Global Taxation, you can streamline the process to file VAT returns, minimize errors, and ensure your compliance with the FTA’s guidelines.

Imagine being able to focus on growing your business without worrying about VAT complexities. Whether you’re handling taxable supplies, aiming to recover AED through a VAT refund, or need assistance filing for zero-rated supplies, Tulpar Global Taxation has you covered. Our experts will guide you every step of the way, helping you file VAT return accurately, validate your data, and comply with the UAE’s VAT regulations. With our support, you’ll have peace of mind knowing your tax obligations are met, enabling you to fully benefit from the UAE’s tax-free opportunities.

Don’t wait until the last moment to file VAT returns! Partner with Tulpar Global Taxation today to simplify your VAT compliance journey and ensure your business stays ahead in 2026. Contact us now for expert advice and reliable solutions tailored to your unique needs.

What is VAT Return?

A VAT return is a crucial document that businesses registered for VAT must submit to the tax authority. It details the VAT on sales (output tax) charged by the business and the VAT paid on purchases (input tax) during a specific return period reference. This return helps businesses calculate their tax liability by comparing the output tax to the input tax. If the output tax is higher, the business must pay the difference. However, if the input tax exceeds the output tax, the business can either claim a refund or carry the excess forward. The VAT return ensures businesses can track their taxable turnover accurately and is submitted via the Federal Tax Authority (FTA) portal using the VAT 201 form.

For businesses with an annual turnover exceeding the mandatory VAT threshold, VAT registration is essential. Once registered, businesses must maintain proper records, including details of sales, to ensure an accurate VAT Return. VAT returns can be submitted on a monthly VAT return basis, depending on the size of the business. Timely submission is crucial for compliance and for managing VAT Payment obligations. It’s important to understand the distinction between taxable turnover and exempt supplies to ensure the correct tax treatment. Each VAT return should reflect the total sales and purchases, with special attention to taxable and exempt supplies.

Submitting your VAT return on time is not only about fulfilling legal obligations; it’s also integral to efficient business operations. Businesses must file their VAT returns based on the VAT return period reference number and ensure all calculations are accurate. A properly filed return helps avoid penalties and simplifies VAT compliance. Whether it’s the end of a quarter or the end of the year, businesses must be ready for the submission deadline and accurately report their output tax to meet the requirements set by the FTA.

How Does VAT Return Work in the UAE?

In the UAE, the VAT return process requires VAT-registered businesses to diligently maintain comprehensive records of all transactions, including sales, purchases, and the corresponding VAT amounts collected and paid. Each tax period, businesses must calculate the total VAT collected from customers (output tax) and the total VAT paid on purchases and expenses (input tax). Using these calculations, they complete the VAT return form “VAT 201,” which is submitted through the Federal Tax Authority (FTA) portal. This form requires detailed entries for sales, purchases, output VAT, and input VAT.

After completing the form, businesses review all entries for accuracy before filing the return electronically. If the output VAT exceeds the input VAT, the business must pay the difference to the FTA. On the other hand, if the input VAT exceeds the output VAT, the business can either request a refund or carry the excess forward to the next tax period.

Timely and accurate filing is essential to avoid penalties and fines. The FTA mandates strict compliance and may conduct audits to verify the accuracy of VAT returns. Therefore, businesses must ensure all records are precise and complete, maintaining transparency and adherence to regulations. This process helps maintain the integrity of the tax system and supports businesses in fulfilling their VAT obligations efficiently.

15 Essential Things To Know Before Filing Your VAT Returns in the UAE

Filing VAT returns in the UAE can be a complex and meticulous process, but understanding the key aspects can simplify it and ensure compliance with the Federal Tax Authority (FTA). Here are 15 essential things to know before filing your VAT returns:

1. What are the Three Categories of VAT?

In the UAE, VAT is classified into three main categories: standard-rated, zero-rated, and exempt.

Standard-rated VAT: This applies to most goods and services at a rate of 5%. Businesses must charge this VAT on their sales and can reclaim VAT on their purchases.

Zero-rated VAT: Certain goods and services, such as exports of goods and services outside the GCC, international transportation, and the first sale of residential property, are taxed at 0%. Although businesses must report zero-rated supplies in their VAT returns, they can reclaim the input VAT incurred on related expenses.

Exempt VAT: Some supplies are exempt from VAT, meaning no VAT is charged, and businesses cannot reclaim the VAT on purchases related to these supplies. Examples include specific financial services, residential real estate (except the first supply within three years of completion), and local passenger transport.

2. Who must File a VAT Return in UAE?

In the UAE, any business or individual registered for VAT must file a VAT return. This includes those who exceed the mandatory registration threshold of AED 375,000 in annual taxable supplies and imports, as well as those who have opted for voluntary registration with annual taxable supplies and imports exceeding AED 187,500. Even if no VAT is due for a specific VAT return period, registered entities must still file a nil return to stay compliant.

3. The Importance of Accurate and Timely VAT Filing

In the UAE, any business or individual registered for VAT must file a VAT return. This includes those who exceed the mandatory registration threshold of AED 375,000 in annual taxable supplies and imports, as well as those who have opted for voluntary registration with annual taxable supplies and imports exceeding AED 187,500. Even if no VAT is due for a specific VAT return period, registered entities must still file a nil return to stay compliant.

4. VAT Return vs. VAT Refunds: What's the Difference?

- VAT Return: This is a periodic report submitted by VAT-registered businesses detailing the VAT collected on sales (output VAT) and the VAT paid on purchases (input VAT). The return calculates the net VAT payable to the FTA or refundable from the FTA. It’s a mandatory filing requirement that ensures businesses report their VAT obligations accurately.

- VAT Refund: A VAT refund occurs when the input VAT (the VAT paid on business-related purchases and expenses) exceeds the output VAT (the VAT collected on sales). In this case, businesses can request the excess amount as a refund from the FTA or choose to carry it forward to offset future VAT liabilities. Refunds help maintain business cash flow and ensure that businesses are not out of pocket for VAT paid.

5. When to File VAT Return in UAE?

The UAE VAT return filing is typically done quarterly or monthly, depending on the size and annual turnover of the business. For most businesses, the standard tax period for the payable tax is quarterly. However, businesses with annual turnovers exceeding AED 150 million are required to file monthly returns.

The specific filing period is determined by the FTA at the time of VAT registration and must be adhered to ensure compliance and avoid penalties for late filing.

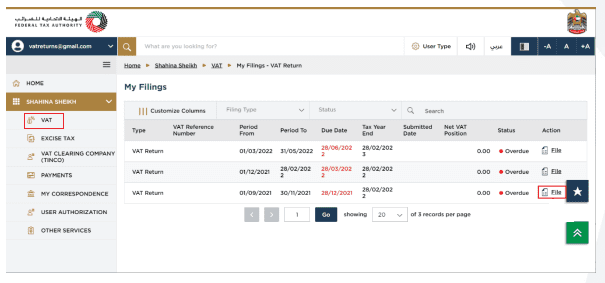

6. How to File a VAT Return in UAE?

To file a VAT return in the UAE, businesses must follow these steps:

Log in to the FTA Portal: Access the Federal Tax Authority’s online portal using your registered credentials.

Navigate to the VAT Returns Section: Locate the section dedicated to VAT returns.

Complete the VAT 201 Form: Enter all required details, including sales, purchases, output VAT, and input VAT. Ensure all values are accurate and supported by documentation.

Review Entries: Double-check all entries for accuracy to avoid mistakes that could lead to penalties or audits.

Submit the Return: Once satisfied with the entries, submit the VAT return electronically through the portal.

Make Payment: If the return shows a net VAT payable, arrange for the payment to be made to the FTA. This can be done through various payment methods available on the portal.

Confirmation: After submission, retain a copy of the confirmation for your records.

7. What is the Standard Tax Period For a Taxable Person in the UAE?

The standard tax time for a taxable person in the UAE can be quarterly or monthly, based on the annual turnover of the business. For most businesses, the taxation period is quarterly, meaning they must file VAT returns every three months.

Businesses with an annual turnover exceeding AED 150 million must file monthly returns. This distinction helps manage the frequency of reporting and ensures that larger businesses, which typically have higher transaction volumes, report their VAT liabilities more frequently. However, keep in mind that there might be cases where the first tax-period can exceed three months.

8. What is the Tax Returns Submission Date?

The tax return submission date is the 28th day following the end of the tax period. For quarterly returns, this means the 28th day after the end of each quarter. For monthly returns, it is the 28th day after the end of each month. If the submission date falls on a weekend or public holiday, the deadline is extended to the next working day. Timely submission is critical to avoid penalties for late filing.

9. VAT Returns on Zero-rated Supplies & Exempt Supplies

- Zero-rated Supplies: These are supplies taxed at 0%. Businesses must still report zero-rated supplies in their VAT return to the FTA. While no VAT is charged to the customer, businesses can reclaim input VAT incurred on related purchases and expenses. Examples include exports and certain healthcare and educational services.

- Exempt Supplies: These supplies are exempt from VAT, meaning no VAT is charged, and businesses cannot reclaim VAT on purchases related to these supplies. Examples include residential property leases and specific financial services. Exempt supplies must be reported in the VAT return, but they do not affect the VAT payable or reclaimable.

10. What Documents Are Required For Filing a VAT Return?

To file a VAT return, businesses must maintain and provide several documents:

Sales Invoices: Detailed records of all sales transactions, including the VAT charged.

Purchase Invoices: Records of all purchases and expenses, including the VAT paid.

Financial Statements: Comprehensive financial records for the tax year.

Import and Export Documents: Documentation of any import and export activities.

Bank Statements: Supporting evidence for transactions.

Credit and Debit Notes: Records of any adjustments to invoices.

Other Supporting Documentation: Any additional records that support the entries in the VAT return.

11. VAT on Sales and all other Outputs

VAT on sales and other outputs refers to the VAT collected from customers on taxable supplies. This includes standard-rated sales and any other transactions where VAT is charged. Businesses must report the total output VAT in their VAT return. Accurate reporting of output VAT is crucial to determining the net VAT payable or reclaimable.

12. VAT on Expenses and all other Inputs

VAT on expenses and other inputs refers to the VAT paid on business purchases and expenses. This includes VAT paid on goods, services, and other business-related expenditures. Businesses can reclaim this input VAT against the output VAT in their VAT return, reducing the net VAT payable. Accurate tracking and reporting of input VAT are essential to ensure proper VAT recovery.

13. Key Sections of Form VAT 201

Form VAT 201 is the standard VAT return form used in the UAE. Its key sections include:

Taxable Person Details: Information about the business, including the VAT registration number and contact details.

Sales and Output VAT: Details of sales transactions and the VAT collected.

Purchases and Input VAT: Details of purchase transactions and the VAT paid.

Adjustments: Any adjustments to the VAT due, such as corrections from previous periods.

Net VAT: Calculation of the net VAT payable or refundable.

Declaration and Submission: Confirmation of the accuracy of the information provided and submission of the return.

14. Who is Exempt From VAT in the UAE?

Certain entities and supplies are exempt from VAT in the UAE. These exemptions include:

Residential Real Estate: The lease or sale of residential property (except the first sale within three years of completion) is exempt from VAT.

Financial Services: Certain financial services, such as life insurance and financial transactions involving interest, are exempt from VAT.

Local Passenger Transport: Transport services provided within the UAE are exempt from VAT.

Bare Land: The sale of bare land is exempt from VAT.

Specific Healthcare and Educational Services: Certain healthcare and educational services may be exempt from VAT, subject to specific criteria and conditions outlined by the FTA.

15. What is the Reverse Charge Mechanism?

The Reverse Charge Mechanism (RCM) in the UAE shifts the responsibility for reporting VAT from the seller to the buyer. It typically applies to cross-border transactions of goods and services.

Under RCM, the buyer records both the input VAT (as if they purchased the goods or services locally) and the output VAT (as if they sold the goods or services) in their VAT return. This mechanism ensures VAT is accounted for in the UAE, preventing tax evasion and simplifying the VAT process for foreign suppliers.

What is the Penalty For Failing to File a VAT Return?

Failure to file a VAT return in the UAE can result in significant penalties for businesses. The filing of VAT returns is a legal requirement for all VAT-registered businesses, and failure to comply with this obligation can lead to financial consequences. The VAT return filing process is vital for reporting VAT on expenses and business transactions, as well as ensuring the correct tax is paid on standard-rated supplies. If a business fails to file its VAT return by the deadline, it risks penalties, which can escalate over time. Businesses are required to submit accurate tax returns based on their financial statements to avoid fines.

Penalties for late or non-submission of VAT returns are imposed by the Federal Tax Authority (FTA) and can vary depending on the length of delay. The penalty structure includes fines for late submissions and for underreporting VAT. For example, businesses that fail to submit a VAT return within a standard tax period (typically quarterly or annually) may face an initial fine. If a taxable business repeatedly fails to comply, the penalties can increase, leading to more severe consequences. Additionally, credit notes and adjustments to previous returns can be impacted if the filing is delayed, making it more challenging to manage your supply chain and tax registration.

How Can Tulpar Global Taxation Help With Your VAT Filing

At Tulpar Global Taxation, we understand that VAT filing can be complex and time-consuming, but it is an essential part of staying compliant with the Federal Tax Authority (FTA) regulations in the UAE. Our experienced team of professionals is here to help you navigate the complexities of VAT compliance, ensuring that your business remains compliant while avoiding penalties and unnecessary complications. We offer tailored services to meet your unique business needs, making sure that VAT return filing is seamless, accurate, and on time.

For businesses in the UAE, VAT filing is not only a legal requirement but also a critical aspect of effective financial management. Incorrect VAT returns can lead to penalties, audit risks, and unnecessary liabilities that can impact your bottom line. With Tulpar Global Taxation, you don’t have to worry about filing inaccurate returns or missing important deadlines. We help you prepare and submit VAT returns accurately, reducing the risks of incorrect VAT returns.

Our VAT experts provide a step-by-step guide to ensure you meet all your VAT liabilities. Whether you’re dealing with supplies subject to VAT, export documents, or residential buildings, we ensure that you accurately report VAT on goods and services. With constant changes in VAT regulations and additional reporting requirements, we make sure your VAT return period remains in compliance, minimizing errors and optimizing VAT recovery. We help you understand and manage the intricacies of monthly filing, debit notes, and financial services that may apply to your specific sector. Our team is equipped to handle incorrect returns or situations involving voluntary registration, customs registration, and even passenger transport services to ensure your filings are precise.

We also offer personalized advice to ensure that business expenses and business details are well-documented for VAT purposes. This helps you maximize your VAT refund and ensures that your business purposes are accurately reflected in your VAT returns. Our experts keep you up to date on the latest regulations regarding UAE VAT Supply of Goods and Services, and we manage any national holiday deadlines for smooth and timely filings.

Simplify VAT Filing with Comprehensive Support

Tulpar Global Taxation Services goes beyond just VAT return filing services. We handle all communication with the Federal Tax Authority on your behalf, reducing your administrative burden so that you can focus on what really matters running your business. Our services extend to managing the online portal, ensuring all your VAT filings are submitted efficiently and without delay. We provide clear, straightforward guidance on the VAT registration certificate and any related business documentation you need to stay compliant. With our support, you don’t have to worry about missing deadlines or navigating complex VAT processes. We make sure your business is in line with accurate reporting practices, and we offer proactive advice on the best ways to manage your VAT affairs.

Trust & Get Timely VAT Filings

At Tulpar Global Taxation, our team of experts helps businesses of all sizes ensure timely VAT filings. We take care of the details, from filing returns to managing additional reporting requirements, so you can stay focused on your core business operations. Our services are comprehensive and designed to minimize errors, protect you from potential penalties, and provide you with clear, actionable insights that optimize your VAT recovery.

Whether you’re looking for guidance on VAT return filing, dealing with UAE VAT, or need help with the VAT return period, trust Tulpar Global Taxation to be your partner in compliance. Contact us today to learn how we can streamline your VAT process and ensure that your filings are timely, accurate, and compliant with the latest tax regulations.

FAQS:

A VAT return is a mandatory report submitted to the Federal Tax Authority (FTA) detailing a business’s VAT transactions for a tax period. It includes output VAT collected on sales and input VAT paid on expenses. Accurate filing is essential to remain VAT-compliant.

All VAT-registered businesses in the UAE, including Mainland and Free Zone companies, must file VAT returns. Filing is required even if there are no sales or VAT payable during the period. Non-filing can lead to penalties.

Most businesses file VAT returns quarterly, while some are required to file monthly based on FTA assignment. The filing frequency is shown in the FTA portal. Missing deadlines results in administrative penalties.

Businesses must prepare sales invoices, purchase invoices, VAT calculations, and reconciliations with accounting records. All figures in the VAT return must match financial data. Poor preparation increases audit risk.

Output VAT is the VAT charged to customers on taxable sales, while input VAT is the VAT paid on business expenses. The difference determines whether VAT is payable or refundable. Correct classification is critical for accurate filing.

Common mistakes include incorrect VAT classification, mismatches with accounting records, and claiming ineligible input VAT. Many businesses also forget to report zero-rated supplies. These errors often trigger FTA audits.

Yes, zero-rated and exempt supplies must still be reported in the VAT return. Zero-rated supplies allow input VAT recovery, while exempt supplies do not. Misreporting affects VAT liability and compliance.

Late or incorrect VAT filing results in penalties and potential FTA scrutiny. Repeated errors may lead to VAT audits. Voluntary disclosure may help correct mistakes if handled properly.

Regular VAT reconciliations, proper documentation, and internal VAT reviews help businesses stay audit-ready. Clean records reduce risks during FTA audits. Preparation is better than correction.

Professional VAT advisors ensure correct calculations, timely filing, and compliance with FTA rules. Working with Tulpar Global Taxation helps businesses avoid penalties, manage audits, and file VAT returns with confidence.