Bookkeeping for Small Business Operating in Dubai - UAE

Table of Contents

Let's Talk

Sign Up For Free Consultation

Bookkeeping for Small Business

Effective bookkeeping is a cornerstone for any small business aiming to achieve financial stability and growth. For small business owners, managing transactions accurately is crucial for tracking cash flow and ensuring that expenses are recorded appropriately. By using robust accounting software, business owners can streamline their small business bookkeeping processes, making it easier to monitor invoices, payroll, and overall financial health. This not only reduces the risk of errors but also provides a clearer picture of the business’s financial position, which is essential for informed decision-making.

A dedicated bookkeeper can provide invaluable support to small business owners, handling daily tasks such as recording transactions and maintaining organized business bank accounts. This professional can ensure that all financial activities are documented accurately, which is essential during tax season. Moreover, efficient bookkeeping practices can help small businesses identify spending patterns and areas for improvement, enabling better management of resources and enhancing profitability. With the right systems in place, small business bookkeeping becomes less daunting and more productive.

For those looking for comprehensive support in managing their finances, Tulpar Global Taxation Services offers specialized bookkeeping and accounting solutions tailored for small businesses. Their expertise ensures that business owners can focus on growing their operations while leaving the intricacies of bookkeeping, such as tracking expenses, managing payroll, and generating financial reports, to the professionals. By partnering with Tulpar Global Taxation Services, small business owners can rest assured that their bookkeeping is handled efficiently, providing peace of mind and allowing them to make strategic decisions based on accurate financial data.

Why Bookkeeping Matters for Your Small Business

Bookkeeping is crucial for small businesses as it lays the foundation for financial stability and growth. By maintaining accurate records of all financial transactions, you gain invaluable insights into your business’s cash flow, expenses, and overall financial health. This clarity enables informed decision-making, helping you identify trends, manage budgets, and ultimately drive profitability. Moreover, effective bookkeeping ensures compliance with tax regulations, reducing the risk of costly penalties and maximizing deductions. In essence, bookkeeping is not just a routine task; it is an essential practice that supports your business’s long-term success and sustainability.

The Foundation of Financial Success

For every small business, effective bookkeeping is not just a luxury; it is the foundation of financial success. A comprehensive bookkeeping system helps you keep track of all financial transactions, providing a clear picture of your business’s financial health. By maintaining accurate records, you can generate crucial financial statements, such as balance sheets and profit and loss statements, which detail your business’s income, expenses, and overall profitability.

Good bookkeeping is essential for managing your business finances efficiently. It allows you to assess your cash flow, monitor business expenses, and identify trends over time. By understanding where your money is coming from and where it’s going, you can make informed business decisions that drive growth. Moreover, bookkeeping is important for ensuring compliance with tax regulations and preparing for tax season, enabling you to avoid penalties and maximize deductions.

Common Mistakes to Avoid

Many small businesses that don’t prioritize bookkeeping often fall victim to common mistakes that can jeopardize their financial health. One significant error is neglecting to track business transactions accurately. Failing to document expenses or income can lead to discrepancies in financial reporting, making it challenging to assess the true performance of your business.

Another frequent mistake is mixing personal and business expenses. This practice can complicate your financial records and lead to inaccuracies in your bookkeeping. It’s vital to maintain separate accounts for your personal and business finances to simplify your bookkeeping tasks and provide clarity in your financial reporting.

Additionally, many small businesses overlook the importance of reconciling their bank accounts regularly. Regular reconciliation helps identify any discrepancies early on, ensuring that your financial statements accurately reflect your business’s performance. By avoiding these pitfalls and implementing effective bookkeeping practices from the beginning, you can set your business up for long-term success and sustainability.

What are the basics of Bookkeeping?

Understanding bookkeeping basics is essential for every small business owner, as it equips you with the knowledge needed to manage your finances effectively. At its core, bookkeeping refers to the systematic recording, categorizing, and tracking of financial transactions, which serves as the backbone of your financial system.

Key concepts include differentiating between income and expenses, comprehending the significance of accounts receivable and accounts payable, and familiarizing yourself with essential financial statements such as the balance sheet and income statement. By grasping these fundamental bookkeeping terms and practices, you empower yourself to maintain accurate financial records, make informed business decisions, and ultimately enhance the financial health of your small business.

Key Terms Every Business Owner Should Know

Understanding the essential bookkeeping terms is crucial for every business owner. Here are some key terms to familiarize yourself with:

- Debit: An entry that increases an asset or expense account and decreases a liability or equity account.

- Credit: An entry that decreases an asset or expense account and increases a liability or equity account.

- Liabilities: What your business owes, including loans and unpaid bills.

- Assets: Resources owned by your business that have economic value, such as cash, inventory, and equipment.

- Accounts Receivable: Money owed to your business for goods or services provided.

- Financial Transactions: Any economic activity that affects the financial position of your business.

Knowing these terms will empower you to navigate your financial records and enhance your understanding of the bookkeeping process. This foundational knowledge is essential for managing your personal finances and your business effectively.

The Difference Between Bookkeeping and Accounting

While bookkeeping and accounting are often used interchangeably, they refer to different functions within your business’s financial management. Bookkeeping is primarily concerned with the accurate recording of financial transactions, including sales, purchases, receipts, and payments. This process lays the groundwork for the financial health of your business.

In contrast, accounting encompasses a broader range of tasks that involve interpreting, classifying, and summarizing financial data. Accountants analyze the information recorded through bookkeeping to prepare financial statements, conduct audits, and provide strategic advice for business growth. Understanding these distinctions is key for managing both business and personal finances effectively and can help you decide when to seek professional help.

Choosing the Right Bookkeeping Method

Choosing the right bookkeeping method is a pivotal decision for small business owners, as it directly impacts how effectively you manage your financial records. There are primarily two methods to consider: single-entry and double-entry bookkeeping. Single-entry bookkeeping is simpler and more straightforward, recording each financial transaction only once, which may be suitable for smaller businesses with uncomplicated financial activities.

On the other hand, double-entry bookkeeping, which records each transaction in two accounts (debit and credit), provides a more comprehensive view of your financial health and helps ensure greater accuracy and accountability. When selecting the best method for your business, consider factors such as the complexity of your financial transactions, your business’s size, and your long-term financial goals. A well-chosen bookkeeping method not only simplifies your bookkeeping process but also enhances your ability to make informed financial decisions that can drive your business’s growth.

Single-Entry vs. Double-Entry Bookkeeping

Choosing the right bookkeeping method is crucial for maintaining accurate financial records and ensuring your business runs smoothly. Single-entry bookkeeping is the simpler of the two methods, where each financial transaction is recorded only once. This method is best suited for smaller businesses with straightforward financial activities, as it requires less effort and is easier to manage. However, it may not provide a comprehensive view of your business finances, making it difficult to track financial health over time.

On the other hand, double-entry bookkeeping involves recording each transaction twice, once as a debit and once as a credit. This method offers a more detailed and accurate picture of your business’s financial status, as it helps you track your accounts receivable, liabilities, and overall financial transactions. Double-entry bookkeeping is essential for businesses that want to scale and require more sophisticated financial reporting.

How to Select the Best Method for Your Business

When deciding on a bookkeeping method, consider the following factors:

- Business Size: Smaller businesses may find single-entry bookkeeping sufficient, while larger or growing businesses may benefit from the robustness of double-entry bookkeeping.

- Complexity of Financial Transactions: If your business involves frequent transactions, multiple revenue streams, or diverse business activities, double-entry bookkeeping may be more appropriate.

- Future Growth Plans: If you plan to expand your business, adopting double-entry bookkeeping from the outset can facilitate future financial management and reporting.

By understanding your specific business needs and accounting preferences, you can choose the most suitable bookkeeping method to support your growth.

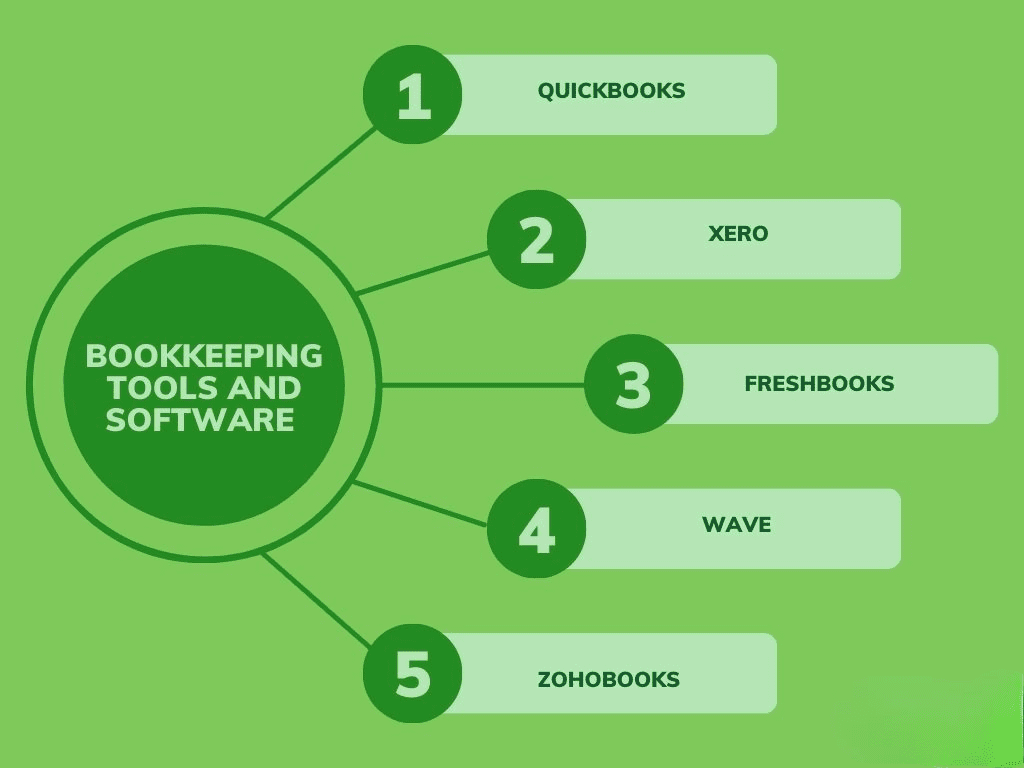

Essential Bookkeeping Tools for Small Businesses

Essential bookkeeping tools for small businesses are vital in streamlining financial management and ensuring accurate record-keeping. With a wide range of software solutions available, business owners can choose tools that best suit their specific needs and budget. Popular bookkeeping software, such as QuickBooks, FreshBooks, and Xero, offer features like automated invoicing, expense tracking, and real-time financial reporting, allowing you to easily manage your finances without the headache of manual calculations.

Additionally, cloud-based bookkeeping solutions provide the flexibility of accessing your financial data from anywhere, facilitating collaboration with accountants and stakeholders. By leveraging these essential tools, small businesses can enhance their bookkeeping processes, reduce errors, and gain valuable insights into their financial performance, ultimately supporting informed decision-making and promoting growth.

Top Software Solutions to Consider

Investing in the right bookkeeping software is essential for streamlining your bookkeeping process and enhancing accuracy. Various software solutions cater to different needs, making it easier to manage your business books efficiently. Some popular options include:

- QuickBooks: This software offers a comprehensive suite of features for tracking income, expenses, invoicing, and generating financial statements. It is particularly suitable for small business accounting.

- FreshBooks: Designed for service-based businesses, FreshBooks simplifies invoicing and expense tracking while providing insights into cash flow and profitability.

- Xero: A cloud-based solution that offers excellent features for collaboration, invoicing, and reporting, making it ideal for businesses looking for real-time financial visibility.

Choosing the right business accounting software can significantly enhance your bookkeeping efficiency and accuracy.

Benefits of Cloud-Based Bookkeeping

Adopting cloud-based bookkeeping solutions offers numerous benefits for small businesses. These systems provide the flexibility to access your financial data from anywhere, making it easier to keep track of your personal and business expenses. Cloud-based solutions often include features such as automatic updates, secure backups, and real-time collaboration, allowing multiple users to access and manage financial data simultaneously.

Additionally, cloud-based bookkeeping significantly reduces the risk of data loss. By securely storing your financial records in the cloud, you can easily recover them in case of unexpected events. Embracing digital bookkeeping not only streamlines your bookkeeping process but also enhances the overall financial health of your small business.

Automating Your Bookkeeping Process

Automating your bookkeeping process can transform the way your business manages its financial records, saving you time and reducing errors. By leveraging advanced accounting software and tools, you can streamline tasks such as data entry, invoice generation, and expense tracking. Automation not only enhances accuracy but also provides real-time insights into your financial health, enabling you to make informed decisions quickly. This shift allows your team to focus on strategic initiatives rather than repetitive tasks, ultimately fostering a more efficient and productive work environment. Embracing automation in bookkeeping is a crucial step towards optimizing your overall financial management.

Save Time and Reduce Errors

Automating your bookkeeping tasks can save you valuable time and minimize the risk of errors. With bookkeeping software, many tasks such as invoicing, bank reconciliation, and expense tracking can be automated. This automation allows you to focus on running your small business rather than getting bogged down in paperwork.

By automating data entry and transaction recording, you can ensure that your financial records are consistently accurate. This reduces the likelihood of common bookkeeping errors, which can lead to discrepancies in your financial reporting and ultimately affect your business decisions.

Streamline Your Workflow with Technology

Using technology to manage your bookkeeping can streamline your workflow significantly. Automation tools help eliminate repetitive tasks, allowing you to establish a more efficient bookkeeping routine. For instance, integrating your accounting software with your bank account can help you track income and expenses in real-time, giving you a clearer picture of your business finances at any moment.

Moreover, leveraging technology for financial reporting allows you to generate accurate reports quickly, enabling you to assess your financial performance and make strategic adjustments as needed. This increased efficiency not only enhances your productivity but also positions your business for growth.

Managing Your Business Finances Effectively

Effectively managing your business finances is crucial for ensuring long-term success and sustainability. This involves not only tracking income and expenses but also implementing strategic budgeting and forecasting practices that align with your business goals. By regularly reviewing financial statements and performance metrics, you can identify trends, spot potential issues early, and make informed decisions about resource allocation.

Additionally, establishing a solid cash flow management system helps maintain liquidity, ensuring that you have the necessary funds to meet obligations and invest in growth opportunities. With a proactive approach to financial management, you can navigate challenges confidently and position your business for future success.

Keeping Accurate Records: Tips and Tricks

Maintaining accurate records of your business transactions is critical for effective financial management. Here are some tips to help you keep your bookkeeping organized:

- Establish a Regular Schedule: Set aside dedicated time each week to update your financial records, ensuring you stay on top of your bookkeeping tasks.

- Categorize Expenses: Create categories for different types of expenses, making it easier to track spending and prepare for tax season.

- Use Consistent Naming Conventions: When labeling transactions, use clear and consistent naming conventions to avoid confusion.

- Reconcile Regularly: Perform monthly reconciliations of your bank accounts to identify discrepancies and ensure your financial statements are accurate.

By implementing these best practices, you can keep your business finances organized and prepare for unexpected challenges.

Preparing for Tax Season with Confidence

Effective bookkeeping is vital when preparing for tax season. Keeping detailed and accurate records of your business activities allows you to approach tax filings with confidence. Here are some strategies to ensure a smooth tax season:

- Track Deductions: Maintain meticulous records of all business expenses, as these can significantly reduce your taxable income.

- Separate Personal and Business Finances: Keep distinct records for personal and business transactions to avoid complications during tax filing.

- Organize Financial Statements: Have your balance sheets and income statements readily available, as they will be necessary for tax preparation.

With a well-organized bookkeeping system in place, you can ensure compliance with tax regulations and maximize your deductions, making tax season much less stressful.

Expert Bookkeeping Services by Tulpar Global Taxation

At Tulpar Global Taxation, we offer expert bookkeeping services designed to streamline your financial management and ensure accuracy in your records. Our team of experienced professionals is dedicated to providing tailored solutions that meet the unique needs of your business, whether you’re a small startup or a larger enterprise. We utilize advanced accounting software and best practices to handle everything from day-to-day transaction tracking to financial reporting and compliance.

By partnering with us, you can free up valuable time and resources, allowing you to focus on core business activities while we manage your bookkeeping efficiently. Trust Tulpar Global Taxation to enhance your financial clarity and support your business’s growth.

Customized Solutions for Your Business Needs

At Tulpar Global Taxation, we understand that every small business has unique bookkeeping needs. Our expert bookkeeping services provide customized solutions that help you manage your financial records effectively. Whether you’re just starting or looking to improve your existing bookkeeping process, our team of professionals can assist you in creating a tailored strategy that aligns with your business goals.

Let Tulpar Handle Your Bookkeeping

Partnering with Tulpar Global Taxation allows you to focus on what you do best running your business. Our experienced team will handle all aspects of your bookkeeping, from transaction recording to financial reporting, ensuring that your financial records are accurate and up-to-date. With our expert services, you can make informed decisions based on reliable financial data, paving the way for your business’s growth and success.

Contact Us Today

Are you ready to take control of your bookkeeping and elevate your business’s financial management? At Tulpar Global Taxation, we understand the unique challenges small businesses face when it comes to managing their finances. That’s why we offer comprehensive bookkeeping services tailored to your specific needs. Our team of experienced professionals is dedicated to helping you streamline your financial processes, ensuring accuracy and compliance while providing you with valuable insights into your business’s financial health.

Contact us today to learn more about how our expert bookkeeping solutions can support your small business in achieving its financial goals. With our assistance, you can simplify your bookkeeping tasks, reduce stress, and enhance your overall financial well-being. Let us take care of the details so you can focus on what matters most growing your business and realizing your vision. Together, we can create a solid foundation for your financial success!

FAQs:

Bookkeeping for small businesses involves recording daily financial transactions such as sales, expenses, payments, and receipts. It ensures accurate financial records that support VAT, Corporate Tax, and regulatory compliance in the UAE. Proper bookkeeping is the foundation of sound financial management.

Yes, UAE laws require businesses to maintain proper accounting records. Even small businesses must keep accurate books to comply with VAT, Corporate Tax, and audit requirements (where applicable). Poor record-keeping can result in penalties and compliance issues.

Bookkeeping helps small businesses track cash flow, control expenses, and make informed decisions. It also ensures smooth VAT return filing and Corporate Tax calculations. Without proper bookkeeping, businesses face higher risks of errors and audits.

Small businesses should maintain sales invoices, purchase invoices, bank statements, expense receipts, payroll records, and general ledgers. These records must be retained for the prescribed period under UAE regulations. Organized records simplify audits and tax filings.

Accurate bookkeeping ensures correct recording of taxable supplies, input VAT, and adjustments. This makes VAT return preparation faster and more accurate. It also reduces the risk of penalties and FTA audits due to errors.

Yes, Corporate Tax calculations are based on financial records maintained through bookkeeping. Accurate income and expense tracking is essential to determine taxable profits correctly. Bookkeeping also supports Corporate Tax registration and filing requirements.

Many small businesses prefer outsourcing bookkeeping to reduce costs and ensure accuracy. Outsourced bookkeeping provides access to expertise without hiring full-time staff. It also ensures compliance with evolving UAE tax regulations.

Popular accounting software includes QuickBooks, Zoho Books, Xero, and Tally. The choice depends on business size, transaction volume, and reporting needs. Professional bookkeepers help select and implement the right system.

Common mistakes include mixing personal and business expenses, poor documentation, delayed recording, and incorrect VAT treatment. These issues often lead to cash-flow problems and compliance risks. Regular bookkeeping reviews help prevent errors.

Experienced accounting and tax professionals provide reliable bookkeeping services tailored to small businesses. Working with Tulpar Global Taxation helps small businesses maintain accurate books, ensure tax compliance, and focus on growth.