Table of Contents

Related Articles

Let's Talk

Sign Up For Free Consultation

Corporate Tax Registration In UAE: A Comprehensive Guide

In October 2023, the United Arab Emirates (UAE) introduced a major transformation in its tax regulations by implementing Federal Decree-Law No. 47 of 2022 on the Taxation of Corporations and Businesses, commonly known as the Corporate Tax Law. This law sets the foundation for corporate tax in UAE, requiring businesses to register and file tax returns through the Federal Tax Authority (FTA). To comply with this law, businesses must undergo the corporate tax registration process and obtain a TRN number.

The Corporate Tax rules applies to various entities, including traditional companies, certain partnerships, unincorporated entities, and natural persons conducting corporate activities in the UAE. Both businesses within free zones and mainland UAE are liable to this law, depending on their nexus in the UAE. Tax year for each taxable person is determined annually, and compliance with corporate tax regulations is mandatory. Businesses need to register for corporate tax through the EmaraTax platform, ensuring their registration details are up to date via the EmaraTax portal. Additionally, tax agents are available to assist in the corporate tax registration application and ongoing tax compliance processes.

Businesses should note that failure to register for UAE corporate tax or meet deadlines for corporate tax returns may result in penalties. Tulpar Global Taxation offers expert assistance to guide you through the UAE corporate tax registration and tax filing processes. Our team ensures compliance with all UAE tax laws, including acquiring the necessary corporate tax registration number, managing permanent establishments in the UAE, and providing support for businesses to register for a corporate tax before the end of the tax year.

By partnering with Tulpar Global Taxation, you’ll receive guidance on understanding your obligations under the corporate tax rule, determining if your business is required to corporate tax, and completing the registration application with the FTA. Our experts help businesses navigate corporate tax in Dubai, ensuring compliance and helping you meet the relevant tax percentage requirements.

Whether you’re a startup or an established corporation, Tulpar Global Taxation will help you navigate the complexities of UAE’s corporate tax registration procedure and ensure that your tax returns are filed accurately. From obtaining your TRN number to managing your corporate taxes, we provide comprehensive support for all your taxation needs. Let us assist you with corporate tax registration in UAE using your UAE Pass and help your business stay controlled in the UAE and compliant with tax requirements.

What is Corporate Tax in the UAE?

Corporate Tax is a direct tax levied by the FTA on the taxable income of corporations, businesses, and certain individuals engaged in business activities within the UAE. This tax, often referred to as “Corporate Income Tax” or “Business Profits Tax” in other regions, is part of the Corporate tax regulations and is applicable to a broad range of UAE businesses. Taxable persons for corporate tax include companies, certain partnerships, unincorporated entities, and individuals that meet the corporate tax goals outlined in the tax framework.

To comply with the UAE Corporate tax regulations, businesses must register for a corporate tax. Tulpar Global Taxation provides expert corporate tax registration services, ensuring businesses comply with FTA requirements. The FTA issues guidance on how businesses can properly register corporate tax in UAE and meet their obligations for tax transparency. The direct tax imposed by the UAE government applies to a company’s net taxable income, and corporate tax goals include ensuring fair taxation based on business profits. Businesses are required to file their tax submissions based on the tax year, which is typically aligned with their financial year, usually spanning 12 months. Payment of corporate tax is due within nine months following the end of the relevant tax year, liable with UAE tax regulations.

The UAE’s corporate tax regime applies to tax year starting on or after June 1, 2023, meaning businesses must be proactive in understanding their obligations under the new tax laws. It is critical to register for a corporate tax within the timeframes set by the FTA. Tulpar Global Taxation offers comprehensive tax services, including the assistance of a qualified tax advisor to help businesses navigate the complexities of the UAE CT regime and meet their tax obligations. Ensure your business is fully compliant with the UAE corporate tax rule by partnering with Tulpar Global Taxation, a trusted provider of corporate tax registration services and expert guidance on all matters related to direct tax and tax transparency.

How Does UAE Corporate Tax rule Work?

The corporate tax supports the UAE’s broader strategy of economic diversification, reducing dependency on hydrocarbon sectors and promoting growth in other industries such as technology, finance, and tourism.

In summary, the Corporate tax regulations in the UAE is designed to create a balanced and sustainable economic environment, fostering growth, fairness, and international alignment while funding essential public services and infrastructure.

The Corporate tax regulations in UAE established under Federal Decree-Law No. 47 of 2022, is a cornerstone of the country’s economic strategy, aimed at fostering fiscal sustainability, promoting economic diversification, and ensuring transparency in business operations. This legislation imposes a 9% tax on the taxable income of entities operating within the UAE, including corporations, partnerships, unincorporated businesses, and individual entrepreneurs with an exemption for income below AED 375,000 to support small and medium-sized enterprises (SMEs) and startups.

Taxable income is determined by subtracting allowable deductions and adjustments from the gross income derived from business operations. These deductions encompass various expenses, such as operational costs, employee salaries, asset depreciation, and interest payments on business loans. The tax year typically aligns with the financial year of the entity, facilitating systematic tax assessment and collection.

The FTA maintains the corporate tax registration procedure, oversees compliance with the Corporate tax regulations, administers the tax regime, issues guidelines, and conducts audits. Non-compliance may result in penalties, including fines and interest charges. Additionally, the UAE has established Double Taxation Agreements (DTAs) with other jurisdictions to prevent the double taxation of income, fostering cross-border trade and investment.

In summary, Corporate tax regulations in UAE plays a vital role in shaping the country’s economic landscape, promoting fairness, transparency, and international cooperation in taxation. By adhering to these regulations, businesses contribute to the UAE’s economic growth and stability while benefiting from a conducive environment for investment and entrepreneurship.

Types of Corporate Tax in the UAE

In the UAE, there are primarily two categories of corporate tax regulations: corporate income tax and value-added tax (VAT).

1. Corporate Income Tax

Corporate income tax is a direct tax levied on the profits earned by businesses operating within the UAE. This tax applies to a wide range of entities and activities, and its implementation reflects the UAE’s commitment to aligning with international tax standards.

Scope of Corporate Income Tax

Taxable Entities: Corporate income tax applies to UAE-incorporated companies, including those in free zones, foreign branches, and certain unincorporated businesses.

Tax Rates: The standard corporate tax percentage is 9% on business profits exceeding a certain threshold, aimed at exempting small businesses and startups from the tax burden.

Exemptions: Certain sectors and types of income are exempt from corporate tax, such as income derived from dividends, capital gains under specific conditions, and qualifying income from certain government entities and non-profit organizations.

Key Features

Annual Filing: Businesses are required to file annual tax submissions detailing their taxable income, allowable deductions, and applicable exemptions.

Tax Period: The tax year is generally the financial year or part thereof for which a tax submission needs to be filed.

Compliance and Penalties: The UAE FTA oversees the administration, ensuring compliance through audits and imposing penalties for non-compliance.

2. Value-Added Tax (VAT)

Value-added tax (VAT) is an indirect tax imposed on the consumption of goods and services. Implemented on January 1, 2018, VAT is part of the UAE’s strategy to diversify its revenue sources away from oil dependency.

Scope of VAT

Taxable Entities: All businesses engaged in the supply of taxable goods and services with annual turnover exceeding the mandatory registration threshold must register for VAT.

VAT Rates: The standard VAT rate is 5%. Certain goods and services may be zero-rated (0%) or exempt, depending on their nature and purpose.

Key Features

Registration: Businesses must register for VAT if their taxable supplies and imports exceed the mandatory registration threshold. Voluntary registration is also allowed for businesses below the threshold.

Invoicing and Collection: VAT-registered businesses must issue VAT invoices for taxable supplies, collect VAT from customers, and remit it to the FTA.

Input VAT Recovery: Businesses can recover the VAT paid on business-related expenses (input VAT), provided they comply with the relevant conditions and documentation requirements.

Filing and Payment: VAT returns must be filed quarterly or monthly, depending on the turnover, and any VAT due must be paid within the specified deadlines.

3. Excise Tax

While not traditionally classified under corporate tax, excise tax is another form of indirect tax that businesses in specific sectors need to be aware of. Introduced in 2017, it targets goods that are harmful to human health or the environment.

Scope of Excise Tax

Taxable Goods: Excise tax applies to products such as tobacco, energy drinks, carbonated drinks, and other items deemed harmful.

Tax Rates: Excise tax percentages vary, typically ranging from 50% to 100% of the retail price, depending on the product.

Key Features

Registration and Reporting: Businesses dealing in excisable goods must register with the FTA, file regular returns, and pay the excise tax due.

Compliance and Penalties: The FTA enforces compliance through audits and imposes penalties for non-compliance, including fines and possible criminal prosecution for severe breaches.

In summary, each of these corporate taxes serves different regulatory and economic purposes, from direct taxation of business profits to indirect taxation on consumption and harmful goods. Understanding these taxes is crucial for businesses operating in the UAE to ensure compliance, optimize tax planning, and contribute to the country’s economic objectives.

Who are Taxable Persons? & Subject to Corporate Tax in UAE

In the UAE, taxable persons liable to corporate tax include a wide range of entities engaged in corporate activities. These persons liable to corporate tax are required to register for the corporate tax and obtain a corporate tax TRN through the FTA. To comply with the UAE’s corporate tax laws, businesses must follow the registration procedure for corporate tax, which includes completing the necessary forms and submitting registration applications for corporate tax using either their credentials or the UAE Pass.

- Companies operating in the UAE, including limited liability companies (LLCs), public joint stock companies (PJSCs), private joint stock companies (PrJSCs), and free zone companies, are all required to apply for corporate tax registration and obtain a TRN for corporate tax. These companies must submit their corporate tax submissions annually, covering the tax filings for a tax year, as specified in the UAE’s tax laws.

- Partnerships like general partnerships (GPs) and limited liability partnerships (LLPs) are also considered taxable persons and need to apply for a tax registration. These partnerships, along with unincorporated entities such as sole proprietorships, must ensure compliance with the UAE corporate tax registration procedure. Self-employed individuals, freelancers, and professionals conducting corporate activities in the UAE are similarly required to register with the FTA and receive a TRN number.

- Branches of foreign companies and permanent establishments (PEs) in the UAE are liable to corporate tax on the profits derived from their UAE operations. These entities must also apply for corporate tax registration and ensure they complete the corporate tax registration procedure before the tax deadlines. The UAE mandates that all businesses operating in the UAE and falling under the category of taxable persons must obtain a TRN number and adhere to the corporate tax UAE regulations.

- The UAE corporate tax percentage is set at 9%, with some industries or entities potentially eligible for specific rates or exemptions. Businesses must register for a corporate tax prior to March 1, 2024, if applicable, and ensure they are meeting international standards for tax transparency. Tulpar Global Taxation provides expert guidance throughout the entire process, helping businesses apply for corporate tax registration, obtain their TRN number, and file accurate corporate tax filings.

By partnering with Tulpar Global Taxation, businesses can navigate the UAE corporate tax regulations efficiently, ensuring compliance with all aspects of corporate tax Dubai, company tax UAE, and tax submissions for a tax year. We ensure that all businesses, whether local or international, are fully registered and compliant with the UAE’s corporate tax registry.

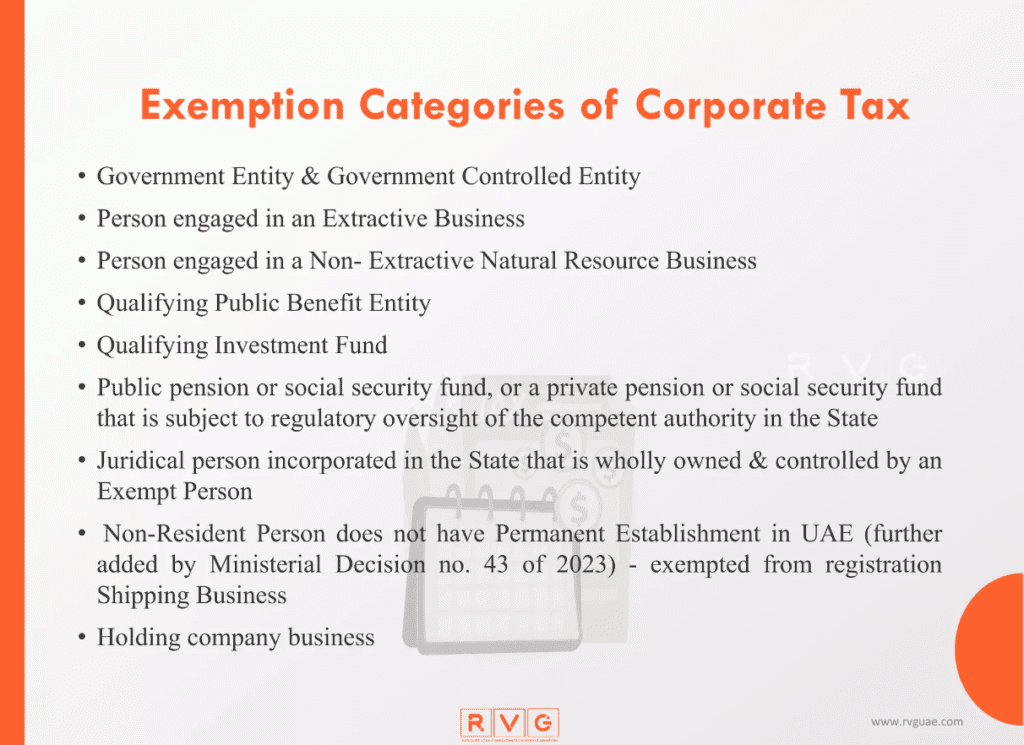

Who Are Exempt from Corporate Tax?

In the UAE, various entities and specific types of income are exempt from corporate tax to foster economic growth, attract foreign investment, and support strategic sectors. Understanding these exemptions is crucial for businesses to navigate the UAE’s tax landscape effectively. Here’s a look at exempt persons from corporate tax in Dubai:

1. Non-Resident Companies

Companies incorporated outside the UAE that do not have a permanent establishment or generate income within the country are generally exempt from corporate tax. This provision aims to attract international businesses to use the UAE as a hub for their operations without being taxed on their global income.

2. Free Zone Entities

Businesses operating within designated free zones such as Dubai International Financial Centre (DIFC), Jebel Ali Free Zone (JAFZA), and Abu Dhabi Global Market (ADGM) can benefit from corporate tax exemptions. These zones offer tax holidays that typically range from 15 to 50 years, liable to renewal. The exemptions are designed to attract foreign direct investment and promote economic activity in specific sectors.

3. Certain Types of Income

Dividend Income: Dividends received by a UAE-resident company from another UAE-resident company may be exempt from corporate tax. This exemption avoids double taxation on corporate profits distributed as dividends.

Capital Gains: Capital gains earned from the sale of shares in UAE-resident companies are often exempt from corporate tax. This exemption encourages investment in the UAE’s corporate sector.

Interest and Other Specified Income: Certain types of interest and specified income may also be exempt, especially if they are earned in contexts that promote economic activities and investments.

4. Government Entities

Federal and Emirate Governments are generally exempt from corporate tax on income derived from government activities. However, commercial activities conducted by these entities may still be dependent to taxation to ensure fair competition with private-sector businesses.

5. Non-Profit Organizations

Non-profit organizations, including charities, foundations, and associations that engage in charitable, religious, educational, or social welfare activities, are typically exempt from corporate tax. These exemptions enable these organizations to direct more resources toward their social and humanitarian missions.

6. Foreign Entities under Double Taxation Treaties (DTTs)

The UAE has signed numerous double taxation treaties with other countries to prevent double taxation of income. These treaties often provide exemptions or reduced tax percentage on certain types of income, such as royalties, dividends, and interest, earned by foreign companies operating in the UAE.

7. SME Exemptions and Thresholds

The UAE may offer specific exemptions or reduced tax percentage for small and medium-sized enterprises (SMEs) based on annual turnover thresholds. This approach supports entrepreneurship and the growth of SMEs by reducing their tax burden during the initial stages of their development.

8. Investment Funds

Investment funds that meet specific criteria, such as those that invest in UAE assets or certain sectors, may be exempt from corporate tax. These exemptions are designed to attract investment and promote the development of the financial services sector.

9. Income from Certain Activities

Agricultural and Fisheries Activities: Income derived from specific agricultural and fisheries activities may be exempt to support the sustainability and growth of these sectors.

Cultural, Artistic, and Sports Activities: Entities involved in promoting cultural, artistic, and sports activities may also qualify for exemptions, encouraging the development of these sectors.

These exemptions are tailored to promote economic growth, attract foreign investment, and support strategic sectors. Businesses operating in the UAE should stay informed about the specific criteria and conditions for these exemptions to ensure compliance and optimize their tax planning strategies.

Incorporated Partnerships vs. Unincorporated Partnerships

Incorporated partnerships and unincorporated partnerships are two distinct forms of business structures that differ significantly in terms of legal status, liability, regulatory requirements, and tax treatment. Understanding these differences is crucial for business owners when deciding on the most suitable structure for their operations.

Incorporated Partnerships

Incorporated partnerships are business entities that have undergone formal registration and incorporation, typically with a government authority or relevant regulatory body. They possess a distinct legal identity separate from their owners.

Key Features of Incorporated Partnerships include:

Legal Entity: An incorporated partnership is a separate legal entity from its partners. It can own property, enter into contracts, and sue or be sued in its own name.

Limited Liability: Partners in an incorporated partnership generally enjoy limited liability, meaning their personal assets are protected from the business’s debts and obligations. Their liability is typically limited to their investment in the partnership.

Regulatory Requirements: Incorporation involves compliance with specific regulatory requirements, including registration with governmental authorities, ongoing reporting, and adherence to corporate governance standards.

Taxation: Incorporated partnerships are often taxed as corporations, meaning the partnership itself pays taxes on its profits. In some jurisdictions, shareholders may also pay taxes on dividends received.

Perpetual Existence: Incorporated partnerships have perpetual existence, meaning they continue to exist even if partners leave or new partners join. The entity remains unaffected by changes in ownership.

Unincorporated Partnerships

Unincorporated partnerships are business structures where two or more individuals engage in business together without formal incorporation. These partnerships are typically based on agreements between the partners.

Key Features of Unincorporated Partnerships include:

No Separate Legal Entity: Unincorporated partnerships do not have a separate legal identity from their partners. The business and its partners are legally indistinguishable.

Unlimited Liability: Partners in an unincorporated partnership have unlimited liability. They are personally liable for the debts and obligations of the business, and their personal assets can be used to satisfy business debts.

Simpler Regulatory Requirements: These partnerships are easier to form and operate, with fewer regulatory and administrative requirements compared to incorporated entities.

Taxation: Income generated by the partnership is typically taxed as the personal income of the partners. The partnership itself does not pay taxes; instead, profits and losses are passed through to the partners.

Limited Lifespan: Unincorporated partnerships often dissolve when a partner leaves or dies, unless an agreement specifies otherwise.

In conclusion, the choice between incorporated and unincorporated partnerships depends on factors such as liability preferences, regulatory tolerance, tax considerations, and business continuity needs. Business owners operating within the UAE must carefully assess their specific circumstances and goals to determine the most suitable structure for their partnership.

What is Taxable Income?

Taxable income refers to the net income of a taxable person that is liable to corporate tax. It is the portion of a business’s or individual’s income that is liable to tax, after accounting for allowable deductions, exemptions, and adjustments. Taxable income is calculated by subtracting allowable deductions and exemptions from the gross income earned during the tax year.

Key components of Taxable income include:

Gross Income: This includes income generated from the core corporate activities, business profits, services rendered, dividends, interest, royalties, and capital gains derived from investments, rental income, and other operational revenues/ earnings.

Allowable Deductions: includes costs incurred in the ordinary course of business, such as salaries, rent, utilities, and supplies, deduction for the wear and tear of tangible assets, interest paid on business loans, bad debts that have been written off as uncollectible, and R&D expenses.

Non-Deductible Expenses: Includes personal expenses not related to the business operations, such as personal travel or entertainment, fines and penalties, and non-business-related expenses.

Exemptions and Adjustments: These include income exempt from tax such as qualifying dividends and capital gains, loss carryforwards, and special allowances.

Taxable income is calculated by subtracting allowable deductions and exemptions from the gross income of a business or individual. The formula is:

Taxable Income = Gross Income – Allowable Deductions – Exemptions + Adjustments

To calculate this, let’s take for instance a manufacturing company with a gross income of AED 10,000,000, Allowable deductions of AED 4,000,000 (including salaries, rent, utilities, and raw materials), Exempt income of AED 500,000 with qualifying dividends and a Loss Carryforward of AED 1,000,000. To calculate this company’s taxable income for the year, we simply calculate:

Taxable Income: AED 10,000,000 – AED 4,000,000 – AED 500,000 – AED 1,000,000 = AED 4,500,000

The taxable income in this case amounts to AED 4,500,000

Tax Periods, Exempt Income & Deductions, and Small Business Relief in the UAE

Tax Year: A tax period in the UAE is the specific time frame during which a taxable person must calculate and report their income to determine the corporate tax due. Typically, the tax year aligns with the financial year of the business.

For most businesses, this is a 12-month period, but it can also be a shorter period if the business starts or ends operations partway through a financial year. Businesses must file their corporate tax filings within nine months of the end of their tax year.

Exempt Income

Certain types of income are exempt from corporate tax in Dubai. These exemptions are designed to encourage investment and economic growth in specific sectors. Exempt income includes:

Dividends: Dividends received from UAE companies and foreign subsidiaries are generally exempt from corporate tax.

Capital Gains: Gains from the sale of shares in a subsidiary are typically exempt, provided certain conditions are met.

Income from Participating Interests: Income from qualifying participations, where the UAE company holds a significant stake in a foreign company, may be exempt.

Income from Overseas Permanent Establishments: Profits from a UAE company’s foreign branches may be exempt if they meet specific criteria.

Deductions

Deductions are expenses that can be subtracted from a company’s gross income to determine its taxable income. The UAE allows several types of deductions to encourage corporate activities and reduce the tax burden:

Operational Expenses: Ordinary and necessary business expenses, such as rent, utilities, salaries, and other operating costs.

Depreciation: A deduction for the wear and tear of business assets over time.

Interest Expenses: Interest paid on business loans can be deducted, liable to certain limitations.

Bad Debts: Specific provisions for debts that are deemed uncollectible.

Research and Development (R&D): Expenses related to R&D activities that contribute to economic development are deductible.

Small Business Relief

Small business relief plays a crucial role in supporting the growth and sustainability of small businesses in the UAE by reducing their corporate income tax burden. In line with the corporate tax regime, small businesses with taxable income below a specified threshold may qualify for relief, which is particularly beneficial in both the mainland and corporate tax UAE free zones. This relief helps small businesses in Dubai and other emirates manage their tax liabilities and comply with corporation tax obligations.

For businesses in the corporate tax in Dubai free zone, relief may come in the form of reduced tax percentages, simplified filing procedures, or exemptions from certain compliance obligations. These benefits are determined by the FTA, so businesses must stay updated on the corporate tax registration deadline and ensure they meet the Corporate Tax Registration Last Date. Detailed records of financial statements, income, expenses, and deductions are necessary to ensure accurate corporate tax filings. Companies that need to register for a corporate tax must follow the process laid out by the FTA corporate tax guidelines. The corporate tax registration in Dubai and the broader corporate tax UAE registration procedure require businesses to meet deadlines and obtain a TRN number. Non-resident juridical persons, foreign entities, and other legal persons conducting business in UAE must also register and comply with the corporate tax percentage regulations.

Tulpar Global Taxation Services offers expert assistance with corporate tax registration and provides a range of corporate tax services tailored to businesses operating in both mainland and free zone areas. Whether you need help with corporate tax for free zone persons, or are seeking advice from a corporate tax consultant, Tulpar Global Taxation can guide you through every step of the process, from meeting the corporate tax registration deadline UAE to accurate corporate tax filing.

Businesses in the UAE can take advantage of small business relief to reduce their tax burden, provided they comply with the Gregorian calendar tax year requirements, and meet the obligations set forth by the FTA. Understanding the regulations for taxable persons and legal entities helps businesses align with the UAE’s corporate tax rules, benefiting from the available relief while ensuring compliance.

How To Register For a Corporate Tax in the UAE

Registering for corporate tax in Dubai involves a series of steps that businesses must follow to ensure compliance with the UAE FTA requirements. Here is a comprehensive, step-by-step guide to help you navigate through this corporate tax registration application process effectively:

Step 1: Determine Eligibility

Before starting the registration proocedure, the first step is to determine if your business is required to register for a corporate tax. Generally, all UAE-resident companies, including those in free zones, foreign companies with a permanent establishment in the UAE, and certain individuals conducting corporate activities, need to register if their taxable income exceeds AED 375,000 per year.

Step 2: Gather Required Documentation

To begin the registration procedure, ensure you have the following documents:

Passport copies of the license owner and shareholders

Emirates ID of the license owner and shareholders

Valid trade license details

Company contact details (email, phone)

Financial statements or audit reports (if applicable)

Bank account details

Contact details of authorized representatives

Memorandum and Articles of Association

Certificate of Incorporation

Step 3: Register on the EmaraTax Portal

Visit the EmaraTax platform on the Federal Tax Authority’s website to create an account or log in using an existing account. Once you’ve logged in, navigate to the corporate tax section. On the dashboard, select “Corporate Tax” from the main menu and click on “Register for a Corporate Tax”. Next, complete the registration form with the following information:

Basic Information: Company name, legal form, trade license number.

Contact Information: Address, phone number, and email.

Business Activities: Nature of corporate activities.

Shareholders and Managers: Details of shareholders and managers, including passport copies and Emirates IDs.

Financial Information: Financial year details, annual turnover, and bank account information.

Step 4: Submit the Application

Once the registration form is completed and all required documents are uploaded, submit your application through the EmaraTax portal. The Federal tax Authority typically processes registration applications within 20 business days.

Step 5: Await Approval

Upon approval, you will receive a TRN from the Federal Tax Authority. This number is your official identifier for corporate tax goals and must be used for filing annual tax submissions and complying with corporate tax regulations in the UAE

Key Deadlines

Businesses must register for corporate tax by specific deadlines based on their license issuance month. For example, companies licensed in January or February must register by May 31, 2024.

The deadline for filing a corporate tax submission is within nine months from the end of the tax year. Failure to register or file on time can result in penalties, including an initial penalty of AED 10,000 for late registration.

Additional Considerations:

Register Early: If you anticipate your business income will exceed AED 375,000, it’s advisable to register early to ensure compliance and to become familiar with the system.

Seek Professional Advice: Given the complexities of tax regulations, consulting a registered tax agent or advisor can be invaluable for navigating the registration process and ensuring ongoing compliance

Top Corporate Tax Terms You Should Know

These terms cover the essential concepts of corporate tax in Dubai, helping businesses navigate the complexities of the tax system effectively.

Understanding corporate tax in Dubai involves familiarizing yourself with a range of terms and concepts. Here are the top terms you should know:

- Corporate Tax: A tax imposed on the income or profits of corporations, calculated based on taxable profits, and paid to the FTA.

- Corporate Tax Returns: The process of filing annual tax submissions with the FTA, which includes reporting the entity’s income, deductions, and corporate tax liabilities.

- Annual Tax Return: The annual submission of a corporation’s taxable income and deductions, in line with the tax year, to determine its tax liability.

- Corporate Tax Liabilities: The amount of tax a corporation owes to the government based on its taxable profits and relevant income, including capital gains and corporate activities.

- Corporate Tax Period: The timeframe during which a corporation’s income and activities are assessed for corporate tax goals, typically aligning with the company’s fiscal year.

- Federal Tax Authority: The government entity responsible for corporate tax regulation, collection, and enforcement, ensuring compliance with tax laws and international standards.

- Tax Registration: The process of registering a business entity with the FTA, mandatory for all corporations operating in the UAE, including those in Free Zones.

- Late Registration: The situation where a business fails to register with the FTA within the stipulated registration period, leading to potential penalties.

- Registration Period: The timeframe provided for corporations to register with the FTA once they meet the criteria for corporate tax obligations.

- Entity Details: Information related to the corporate structure, such as trade license details, entity type, and corporate activities, required during tax registration and return filing.

- Trade License: A legal document required for conducting business in the UAE. The trade license details must be provided when registering for corporate tax.

- Branch Details: Information about a corporation’s foreign branches or additional offices that must be declared for tax goals.

- Connected Persons:

Individuals or entities linked to the business that may affect the corporation’s tax obligations, including shareholders, partners, and related parties.

- Concerned Person:

Any individual responsible for fulfilling a corporation’s tax obligations, including filing returns, paying liabilities, and ensuring compliance.

- Foreign Jurisdiction:

A country other than the UAE where a corporation may conduct business or have taxable income, which could impact its corporate tax obligations.

- Resident Juridical Persons:

Entities incorporated or registered in the UAE, required to comply with corporate tax regulations and tax submission to the FTA.

- Non-Resident Person:

An individual or entity not meeting the residency criteria in the UAE but conducting corporate activities that may be liable to corporate tax.

- Exempt Persons:

Individuals or entities excluded from specific corporate tax obligations under UAE law, including certain Free Zone Persons or qualifying public benefit entities.

- Natural Persons:

Individuals, as opposed to corporations, who may be liable to personal income tax, rather than corporate tax, on employment income.

- Resident Person:

An individual or entity meeting the UAE’s residency criteria for tax goals and required to comply with corporate tax obligations.

- Juridical Person:

An entity recognized by law as having its own legal identity, separate from its owners, and liable to corporate tax on its taxable profits.

- Corporate Tax for Free Zone:

Special tax regulations that apply to entities operating within designated Free Zones in the UAE, which may provide tax exemptions or incentives.

- Taxable Income:

The portion of a corporation’s income subject to taxation, calculated after allowable deductions for corporate tax goals.

- Taxable Entities:

Businesses or organizations liable to corporate tax, including corporations, independent partnerships, and other legal entities in the UAE.

- Consolidated Return:

A combined corporate tax submission by a parent company for itself and its subsidiaries, consolidating their taxable income and deductions.

- Filing Returns:

The process of submitting corporate tax submission to the FTA, detailing the company’s income, deductions, and tax liabilities for the tax year.

- Foreign Branches:

Overseas operations of a corporation, whose income may be liable to corporate tax depending on the tax treaties and local regulations.

- Accounting Firms:

Professional service providers specializing in corporate tax, auditing, and financial reporting, who assist businesses with tax submission and compliance.

- Filing Deadline:

The last date by which a corporation must submit its corporate tax to avoid penalties for late filing.

- Administrative Requirements:

The procedural obligations corporations must fulfill to comply with corporate tax rules, including registration, filing returns, and reporting income.

- Regulatory Requirements:

Legal obligations set by the Federal Tax Authority or other UAE authorities, ensuring corporations meet standards for tax transparency and compliance.

- Profit of Corporations:

The financial gains of a corporation after deducting expenses, liable to corporate tax under UAE law.

- Taxable Profits:

The income of a corporation that is subject to taxation after all allowable deductions and exemptions have been applied.

- Corporate Tax Assessment:

The evaluation of a corporation’s taxable income, deductions, and tax liability by the FTA.

- Financial Reporting Standards:

International and UAE-specific standards governing how corporations must report their financial activities for tax goals.

- VAT Payments:

Payments made by businesses in the UAE as part of the Value Added Tax (VAT) system, distinct from corporate tax obligations.

- Input Fields:

Specific sections on tax forms where corporations must input information such as income, deductions, and contact details during tax return submission.

- Corporate Tax Advisors:

Tax professionals who provide guidance and support to corporations on compliance, filing, and tax planning strategies.

- Tax Refund Requests:

Requests submitted to the Federal Tax Authority by corporations seeking a refund for overpaid company taxes.

- Tax Professionals:

Experts in taxation who help businesses navigate Corporate taxation regulations, file returns, and ensure compliance with regulatory requirements.

- Entities Subject:

Businesses or organizations that fall under the jurisdiction of the UAE corporate tax framework and are required to file returns and pay taxes.

- Independent Partnerships:

Business entities operating independently of corporate structures, which may be liable to corporate tax depending on their corporate activities.

- Real Estate:

Property and land investments that may generate taxable income or capital gains for corporations, liable to corporate tax.

- Standards for Tax Transparency:

International guidelines that promote openness in tax reporting and ensure corporations adhere to regulatory requirements.

- Strategic Objectives:

The long-term business goals set by corporations, which may influence tax planning strategies to align with corporate tax liabilities.

- Tax-Free Haven:

A jurisdiction with favorable tax laws where corporations may benefit from reduced tax liability, such as Free Zones in the UAE.

- Tax Registration Certificate:

A document issued by the Federal Tax Authority certifying that a business has successfully registered for corporate tax.

- Tax Haven Company:

A corporation established in a tax-free jurisdiction to reduce its corporate tax liabilities through legal means.

- Allowable Deductions:

Expenses that a corporation is permitted to subtract from its taxable income, reducing the overall tax liability.

- Contact Details:

Information provided during the tax registration procedure or when filing returns, including the authorized signatory’s details and corporate headquarters.

- Corporate Tax Advisors:

Professionals who assist businesses in understanding and fulfilling their tax obligations, including filing returns and managing tax liabilities.

- Authorized Signatory:

The individual responsible for signing tax returns and official documents on behalf of the corporation.

- Relevant Tax Year:

The specific timeframe for which a corporation’s taxable income and corporate tax liabilities are assessed.

- Business Days:

Days of operation for businesses when they can conduct activities, meet tax deadlines, and interact with the Federal Tax Authority.

- Business Goals:

The overall objectives of a corporation, which influence tax planning and strategy to optimize corporate tax outcomes.

- Business Owners:

Individuals or entities that own a corporation and are responsible for fulfilling the company’s corporate tax obligations.

- Time Frame:

The period within which businesses must complete tasks such as registration and filing returns to avoid penalties.

- Additional Time:

Extra time granted by the Federal Tax Authority for businesses to comply with corporate tax requirements, usually to avoid penalties for late filing.

Tulpar Global Taxation Services is here to assist with all aspects of corporate tax compliance, from registration to filing returns. Our expert tax advisors ensure your corporation meets all regulatory requirements while optimizing tax strategies to align with your business goals. Contact us today to learn how we can help you navigate the UAE’s corporate tax landscape.

How Can Tulpar Global Taxation Help You With Your Corporate Tax Registration in the UAE

Tulpar Global Taxation is a leading auditing firm in Dubai, specializing in taxation, accounting, and auditing services. They offer a comprehensive range of services, including tax agency support, corporate tax registration, and tax consultation. Their expertise covers company tax submission, corporate tax liabilities, and financial reporting standards, helping businesses comply with the UAE’s regulatory requirements.

How Tulpar Global Taxation Can Assist with Corporate Tax Registration:

- Entity Details and Registration:

Tulpar Global Taxation ensures your corporation tax registration is handled with precision. They assist in providing the correct entity details, including trade license details, branch details, and other mandatory fields such as business goals and types of income. For foreign branches, they ensure the smooth submission of all relevant application for registration forms.

- Compliance with the Federal Tax Authority (FTA):

Tulpar Global Taxation ensures your company’s tax activities comply with Federal Tax Authority (FTA) regulations and international standards. They help with the preparation and filing of corporate tax, annual returns, and ensure that VAT payments are accurate. Their experts can handle Filing Returns and monitor deadlines to avoid any penalties.

- Corporate Tax Liabilities and Taxable Profits:

With expertise in assessing corporate income tax, taxable entities, and corporate tax liabilities, Tulpar Global Taxation helps optimize your company’s tax obligations. Their specialists ensure your taxable profits, including capital gains and exception of income, are reported accurately in compliance with corporate tax assessment rules.

- Expert Tax Planning and Risk Assessment:

Tulpar Global Taxation offers comprehensive risk assessment and corporate tax alignment assessments. They assist business owners and authorized signatories by aligning tax strategies with strategic objectives and corporate activities, including real estate investments and independent partnerships. By focusing on the profit of corporations, they offer tailored tax planning services, which can minimize additional tax liabilities.

- Tax Registration and Documentation Support:

Tulpar Global Taxation handles all aspects of Tax Registration, including late registration, ensuring your registration period is met. They prepare necessary documentation, including financial statements and company incorporation records, and assist with application submission. They also monitor the earliest issuance of registration certificates and communicate with the Federal CT authorities on behalf of concerned persons or connected persons.

- Consolidated Tax Returns for Corporations:

For large corporations or those with multiple branches, Tulpar Global Taxation assists with consolidated returns. They ensure all corporate income tax for taxable entities is consolidated and reported in one corporate tax return, saving time and reducing administrative burdens.

- Compliance with Administrative and Regulatory Requirements:

Tulpar Global Taxation ensures compliance with administrative requirements and regulatory requirements. From tax-related input fields to ensuring standards for tax transparency and corporate tax year are met, they take charge of the entire process, including handling additional time requests if needed.

- Corporate Tax for Free Zones and Exceptions:

Companies operating in tax-free havens like Free Zones benefit from Tulpar Global Taxation’s specialized services. They help you navigate Corporate Tax for Free Zone guidelines while considering exceptions for specific types of income, such as employment income or relevant income.

- Ongoing Compliance and Support:

Once registered, Tulpar Global Taxation provides ongoing support to meet the filing deadlines for corporate tax returns. They also assist with tax refund requests, manage additional tax liabilities, and ensure compliance with financial reporting standards. Businesses can rely on their expert corporate tax advisors and tax professionals for continuous guidance.

- Real Estate, Business Activities, and More:

Tulpar Global Taxation helps corporations manage their corporate activities, including real estate holdings and access to business reports. They ensure compliance with standards for tax transparency and handle specific situations such as late registration or requesting additional time to complete tasks.

- Ongoing Monitoring and Reporting:

Tulpar Global Taxation monitors the tax year and ensures all business days are utilized effectively for tax reporting. By working closely with accounting firms, they offer insights into business structures like sole proprietorship, ensuring that both large and small corporations meet their tax obligations on time.

- Tailored Solutions for UAE and Abu Dhabi Corporations:

Whether based in Dubai or Abu Dhabi, Tulpar Global Taxation tailors its services to meet specific corporate needs. Their experts in corporate tax alignment assessments ensure that business owners can focus on growth, while Tulpar manages all aspects of tax compliance.

Partner with Tulpar Global Taxation for Tax Compliance Success: With a commitment to high standards, Tulpar Global Taxation Services offers full support for corporate tax registration, tax planning, and compliance with corporate returns. Contact them today to ensure your corporation meets UAE tax regulations and optimizes its financial standing.

Contact Us:

- Website: www.tulpartax.com

- Email: info@tulpartax.com

- Phone: +971-54 444 5124