Share

Table of Contents

The Value Added Tax (VAT) was introduced in the United Arab Emirates (UAE) by the Federal Tax Authority (FTA) on January 1, 2018, as a key component of the nation’s tax system. This initiative aims to generate significant revenue for the government and support economic diversification. The standard VAT rate for most goods and services is set at 5%. However, there are notable exceptions where certain goods and services may qualify for a 0% rate or be entirely exempt from tax.

Given these exceptions and special conditions, many business owners have questions about VAT registration in the UAE, including how it operates, how to accurately calculate VAT for compliance, and understand the VAT registration threshold. In this blog post, we will cover everything you need to know about VAT registration in the UAE.

What is a Value Added Tax (VAT)

Value Added Tax (VAT) is a form of indirect tax that is imposed on the value added to goods and services at each stage of production or distribution. It is a consumption tax, meaning that the ultimate burden of the tax falls on the final consumer who purchases the goods or services.

Unlike direct taxes, which are paid directly to the government by individuals or organizations based on their income, VAT is an indirect tax collected by businesses on behalf of the government. In the UAE, VAT applies to most transactions involving goods and services, with certain exemptions and special treatments.

Overview of VAT in the UAE

The Value Added Tax (VAT) in the UAE is a consumption tax introduced on January 1, 2018, to generate significant government revenue and diversify the economy. This tax is levied on the value added to goods and services at each stage of production and distribution, with the final burden resting on the end consumer. Businesses in the UAE act as tax collectors on behalf of the government, ensuring that VAT is collected and remitted properly.

The VAT rate in the UAE is set at 5%. This standard rate applies to most goods and services, with some exceptions. Certain goods and services may qualify for a 0% VAT rate or be exempt from VAT altogether. For example, specific healthcare and educational services, as well as exports outside the GCC, are often subject to a 0% VAT rate. Conversely, residential properties, bare land, and some financial services are typically exempt from VAT.

In practice, VAT in the UAE operates through a system of input and output taxes. Businesses charge VAT on their sales (output tax) and pay VAT on their purchases (input tax). They are required to file regular VAT returns, usually quarterly, where they report the amount of VAT collected and paid. Any difference between the output tax and input tax must be settled with the Federal Tax Authority (FTA). Compliance with VAT regulations involves accurate record-keeping and timely submission of VAT returns to avoid penalties.

Who Should Register for VAT in the UAE?

In the UAE, VAT registration is divided into two categories: mandatory and voluntary. Understanding these categories helps businesses determine their obligations and potential benefits regarding VAT registration.

Mandatory VAT Registration

In the UAE, resident and non-resident businesses must register for VAT if their taxable supplies and imports exceed the mandatory registration threshold of AED 375,000 per year. This threshold ensures that businesses with significant turnover contribute to the tax system. Taxable supplies encompass all goods and services that are subject to VAT at either the standard 5% rate or the 0% rate, with the exception of those categorized as exempt supplies.

Voluntary VAT Registration

Businesses whose taxable supplies and imports exceed the voluntary registration threshold of AED 187,500 but do not reach the mandatory registration threshold of AED 375,000 can opt for voluntary VAT registration. Voluntary registration can offer several advantages, including the ability to reclaim VAT on business expenses and enhance the business’s credibility.

However keep in mind that irrespective of the VAT registration category you qualify for, you must regularly and accurately keep records, file tax returns, and make prompt payments of VAT dues to ensure compliance with VAT regulations.

VAT Exemptions & Penalties in the UAE

VAT Exemptions in the UAE

In the UAE, certain goods and services are exempt from VAT, meaning no VAT is charged on their supply. These exemptions aim to reduce the tax burden on essential sectors and promote social welfare.

Key Exemptions include:

Residential Properties: The supply of residential properties, whether through sale or lease, is generally exempt from VAT. However, this exemption does not apply to the first supply of a new residential property within three years of its construction, which is zero-rated.

Bare Land: Sales or leases of bare land, meaning land that is not covered by completed buildings or civil engineering works, are exempt from VAT.

Local Passenger Transport: Transport services for passengers within the UAE, such as taxis, buses, and trains, are exempt from VAT.

Certain Financial Services: Financial services provided without an explicit fee, commission, discount, or rebate, such as interest on loans, are exempt from VAT.

These exemptions help maintain affordability and accessibility in critical areas like housing, transportation, and essential financial services.

VAT Penalties in the UAE

The Federal Tax Authority (FTA) imposes penalties for non-compliance of VAT-registered businesses in the UAE to ensure proper adherence and accountability. These penalties are designed to encourage timely and accurate reporting and payment of VAT.

Types of Penalties:

Late Registration: Failure to register for VAT on time can result in a penalty of AED 20,000.

Late Filing of VAT Returns: Submitting VAT returns after the due date can incur a fine of AED 1,000 for the first offense and AED 2,000 for subsequent offenses within 24 months.

Late Payment of VAT: Not paying the due VAT on time can result in a late payment penalty of 2% of the unpaid tax immediately, an additional 4% if not paid within seven days, and a daily penalty of 1% of the unpaid tax after one month, up to a maximum of 300%.

Incorrect VAT Returns: Filing inaccurate VAT returns can lead to a penalty of up to 50% of the underpaid tax amount, depending on the nature and severity of the error.

Failure to Keep Records: Not maintaining proper records can result in a penalty of AED 10,000 for the first offense and AED 50,000 for repeated offenses.

These penalties highlight the importance of compliance with VAT regulations, emphasizing the need for businesses to ensure accurate and timely registration, filing, and payment of VAT.

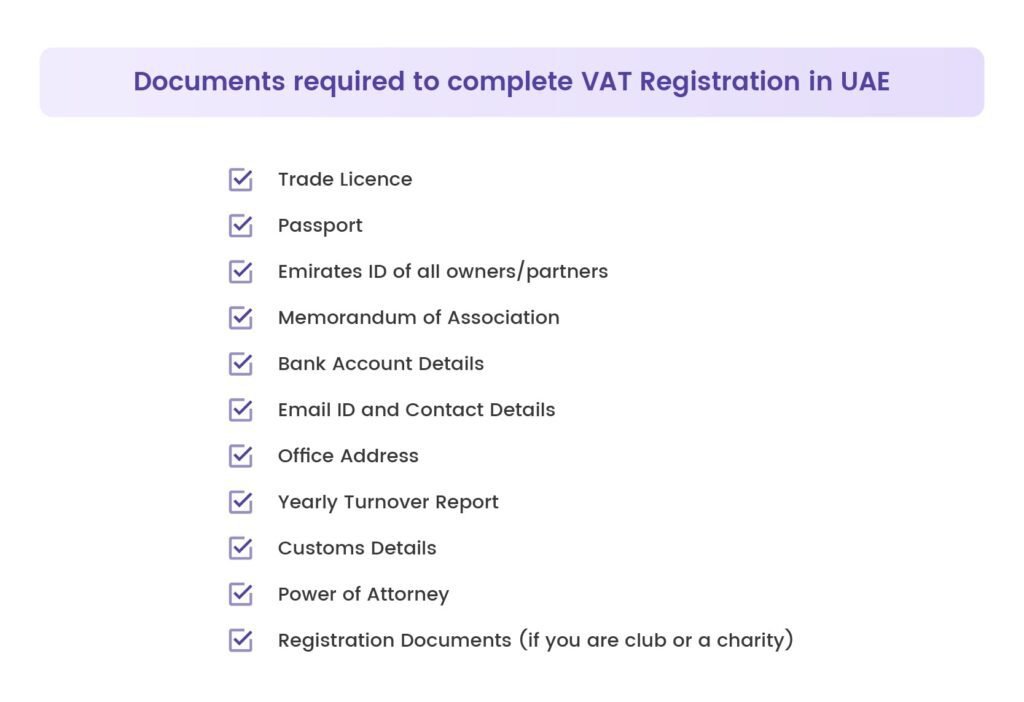

Documents Required For VAT Registration in the UAE

When applying for VAT registration in the UAE, businesses need to prepare and submit certain documents to the Federal Tax Authority (FTA). These documents are essential to complete the VAT registration process and ensure compliance with VAT regulations.

Trade License: A copy of the trade license issued by the relevant UAE authorities, demonstrating the legal status of the business.

Emirates ID: Copies of Emirates IDs for all partners, shareholders, or legal representatives of the business entity.

Passport Copy: Copies of the passport for all partners, shareholders, or legal representatives of the business entity.

Memorandum of Association (MOA): A copy of the MOA, which outlines the objectives and activities of the business as per its registration.

Financial Statements: Audited financial statements for the last 12-month period (if available), providing an overview of the business’s financial position.

Bank Account Details: Details of the business’s bank account, including the IBAN and a recent bank statement.

Contact Information: Complete contact details for the business entity, including physical address, email address, and phone number.

Partnership Agreement: For partnerships, a copy of the partnership agreement is required.

Articles of Association: For companies, copies of the Articles of Association are necessary.

Lease Agreement: A copy of the lease agreement for the business premises, confirming the physical location of operations.

Customs Registration Certificate: For businesses involved in importing goods, a copy of the customs registration certificate may be required.

Power of Attorney: If a legal representative is appointed to handle VAT registration on behalf of the business, a copy of the power of attorney must be provided.

How to Apply for VAT Registration in UAE

Applying for VAT registration in the UAE involves several steps to ensure compliance with the tax regulations. Here’s a general overview of the process:

Check Eligibility: Confirm that your business meets the criteria for mandatory registration. Currently, businesses with taxable supplies and imports exceeding AED 375,000 per year must register for VAT.

Create an Emaratax Account: You need to create an EmaraTax account through the Federal Tax Authority’s (FTA) website and activate it, which is used for all VAT-related transactions.

Gather Required Documents: Prepare necessary documents, including:

Trade license and certificate of incorporation

Passport copies of business owner(s) and authorized signatories

Emirates ID copies of the business owner(s) and authorized signatories

Bank account details

Details of business activities and expected turnover

Form Completion: Access your Emaratax account and complete the online VAT registration form. The form will prompt you to provide details about your business activities, turnover, and bank information.

Application Submission: After filling out the form, review it for accuracy, then finalize and submit your VAT registration application.

Payment: Follow the instructions on the FTA website regarding the fee amount and payment methods. If required, proceed to pay the VAT registration fee.

Supporting Documentation: Include necessary supporting documents as specified by the FTA. These documents assist in verifying the information provided in your application.

Application Review: The FTA will carefully review your application. Upon approval, if you meet the VAT registration requirements in the UAE, you will receive a Tax Registration Number (TRN) and a VAT Certificate. These documents are essential for identifying your VAT registered business for tax purposes. The typical timeframe for completing the VAT registration process is approximately 30 days.

How To Calculate Your VAT in UAE

Here’s how you calculate VAT in the UAE:

Formula

To calculate VAT amount:

VAT Amount =Taxable Amount x VAT Rate

Where:

Taxable Amount: The selling price or value of goods/services subject to VAT.

VAT Rate: Currently 5% (0.05) in the UAE.

Example Calculation

Example 1: Calculating VAT Amount Suppose the selling price of goods or services is AED 1,000

VAT Amount = 1,000 × 0.05

VAT Amount = 50

Therefore, the VAT amount payable is AED 50.

Registering for VAT Tax As a Group

Registering for VAT tax as a group in the UAE involves consolidating multiple businesses under a single registration. The VAT Registration process for a group includes:

Eligibility Check: Ensure each entity within the group meets the UAE’s VAT registration criteria based on turnover and taxable supplies.

Group Structure Confirmation: Identify the controlling entity responsible for submitting the group VAT registration application.

Application Submission: Submit a formal request for group VAT registration to the Federal Tax Authority (FTA), detailing all entities included and their respective details.

FTA Review: The FTA will review the application to verify compliance with VAT regulations and may request additional documentation.

Approval and Registration: Upon approval, the FTA will issue a Group VAT Registration Certificate. Each entity within the group receives a unique Tax Registration Number (TRN), allowing them to operate under the group registration for VAT purposes.

Ongoing Compliance: Maintain accurate records, file consolidated VAT returns, and ensure compliance with VAT obligations as a group entity.

Conclusion

In summary, VAT registration in the UAE involves following clear steps to meet tax requirements. By filling out the registration form accurately, submitting necessary documents, and adhering to FTA guidelines, businesses can obtain their Tax Registration Number (TRN) and VAT Certificate. This process ensures compliance with tax laws, helps manage VAT responsibilities effectively, and supports the UAE’s economic goals. Staying updated on VAT regulations and seeking professional advice when necessary are key to navigating this process smoothly.

Frequently Asked Questions (FAQs)

Taxable supplies refer to goods or services that are subject to VAT in the UAE. This includes sales and imports of goods or services that are not specifically exempt or zero-rated under VAT regulations. Businesses must charge VAT on taxable supplies and include it in their invoices.

Businesses can generally reclaim VAT paid on goods and services purchased for use in their taxable activities. This process is known as input tax recovery. However, there are conditions and restrictions on what VAT can be reclaimed, such as ensuring the purchases were used for business purposes and were not for personal use or exempt activities.

Yes, businesses can request to cancel their VAT registration in the UAE under certain circumstances, such as if they no longer meet the mandatory registration threshold or if they cease trading. The cancellation process involves submitting a request to the Federal Tax Authority (FTA) along with supporting documentation. Once approved, the FTA will cancel the VAT registration and issue a confirmation of cancellation. It’s important to comply with all VAT obligations until the cancellation process is completed.